Commonly, people look at saving and investing as being one in the same. However, both utilise a different approach and way of thinking.

Saving is keeping some of your disposable income to achieve a short-term goal, it takes a conservative method that involves very little risk with your money.

Conversely, investing, takes a higher degree of risk in achieving your longer-term goals. This requires you to invest in growth assets that have the potential to build your wealth. Despite growth assets being more volatile over the short term, they have historically provided higher long-term yields and may be more tax-effective than other asset classes

1. Compound Returns

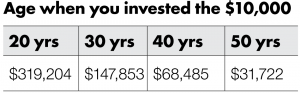

This strategy uses compounding to help accumulate your earnings. By re-investing the earnings you receive from your investment, this enables you to convert your earnings into capital so you can earn more money in the future. To get the most out of compounding, it is important that you give your money time to grow. Over several years, compounding can make a big difference to your wealth. For example, if you invest $10,000 at 8% p.a. until age 65, the table below depicts the difference in investing for longer.

2. Growth Assets to Make Your Money Work Harder

2. Growth Assets to Make Your Money Work Harder

Investing in growth assets like shares, enables your capital the potential to grow over the long term and outpace inflation. Your dividend income may increase over time as share prices rise and the imputation credits that often come with dividend from Australian shares can be used to reduce your tax bill. However, shares can be volatile over the short term.

3. A Balanced Approach

Strategies of a successful investors usually set lifestyle and financial goals, diversify their investment into each of the main asset classes and resist the temptation to switch their money around based on short-term performance. This is considered a balanced approach to investing, you should consider sticking with a balanced mix of assets than chasing past performance.

4. Dollar Cost Averaging

Dollar cost averaging involves investing a fixed amount at regular intervals over a period of time, this can work particularly well with managed investments. Assuming you invest a set amount in a managed investment each month, you can buy more units when prices fall and fewer units when prices rise. As a result, you can average the price you pay for investments and potentially profit from a fluctuating market.

5. Income Splitting

It’s no secret that tax can eat away at your investment returns. However, there is a simple way to ensure you don’t pay more tax than you have to. This strategy places investment assets in the name of your partner (or another family member). The advantage of this strategy is that the owner is required to pay tax on any income and capital gains from the investment. If he/she is on a lower tax rate than you, you may be able to minimize your household tax bill by purchasing all new investments in your partner’s name. If you currently own the investment yourself, you are able to split income by transferring ownership of the investments to your partner (capital gains tax and stamp duty could be payable).